Withholding Tax for Agents

A 2% Withholding Tax (WHT) will be imposed to agents, dealers and distributors whose commissions surpasses RM100,000 within 1 year.

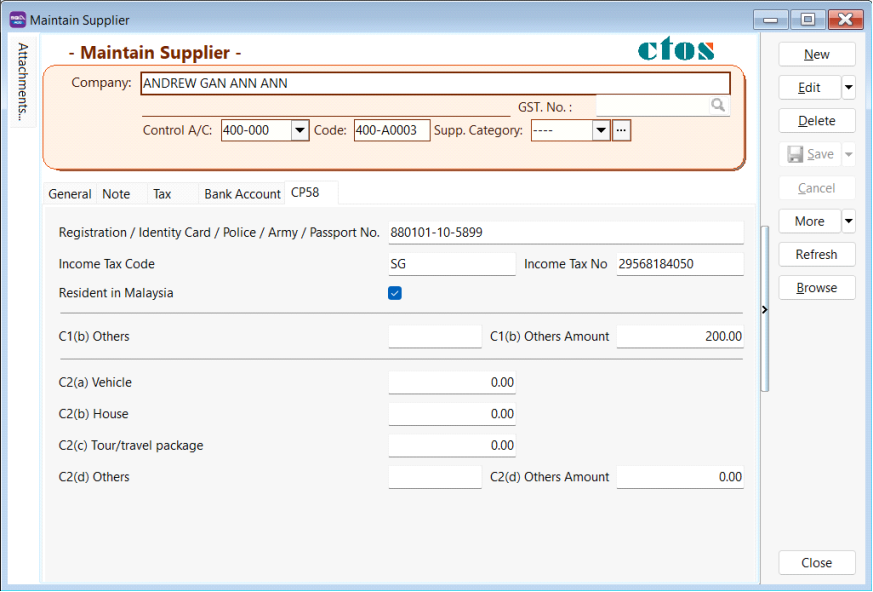

Go to Supplier > Maintain Supplier, you can fill up the agents information such as IC number, Income Tax Number and others information in CP58.

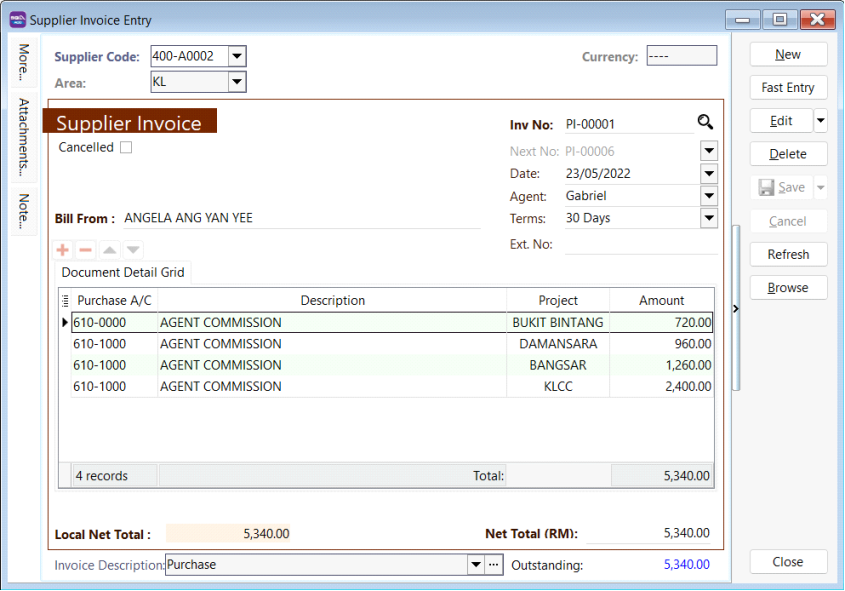

Issue invoices for agent commission from Supplier > Supplier Invoice.

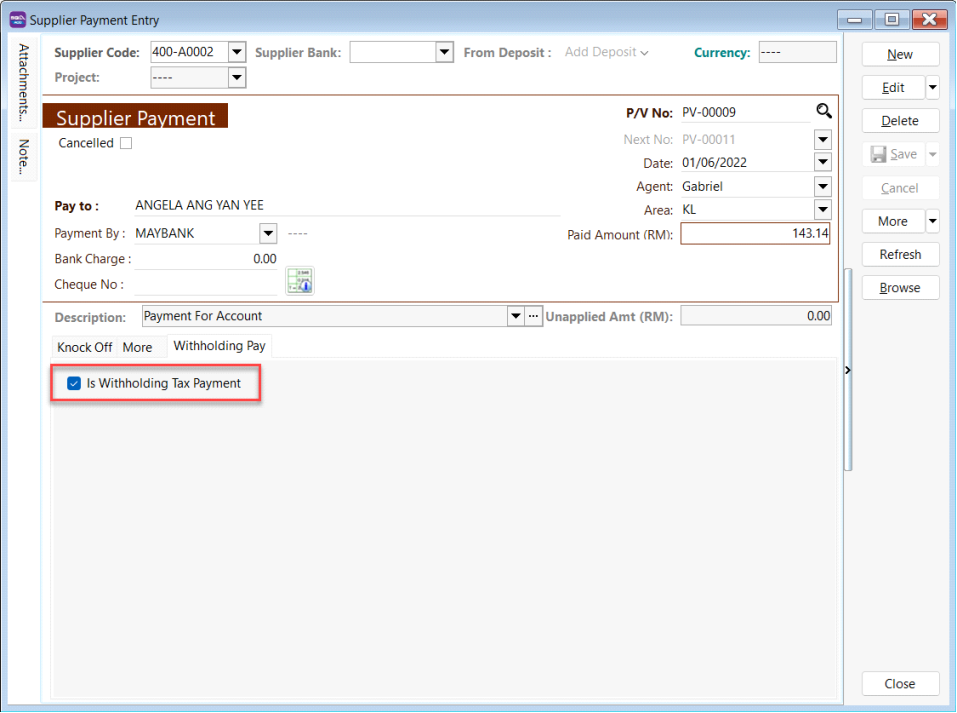

For payment to agent, go to Supplier > Supplier Payment, insert the amount and information, tick on withholding tax payment.

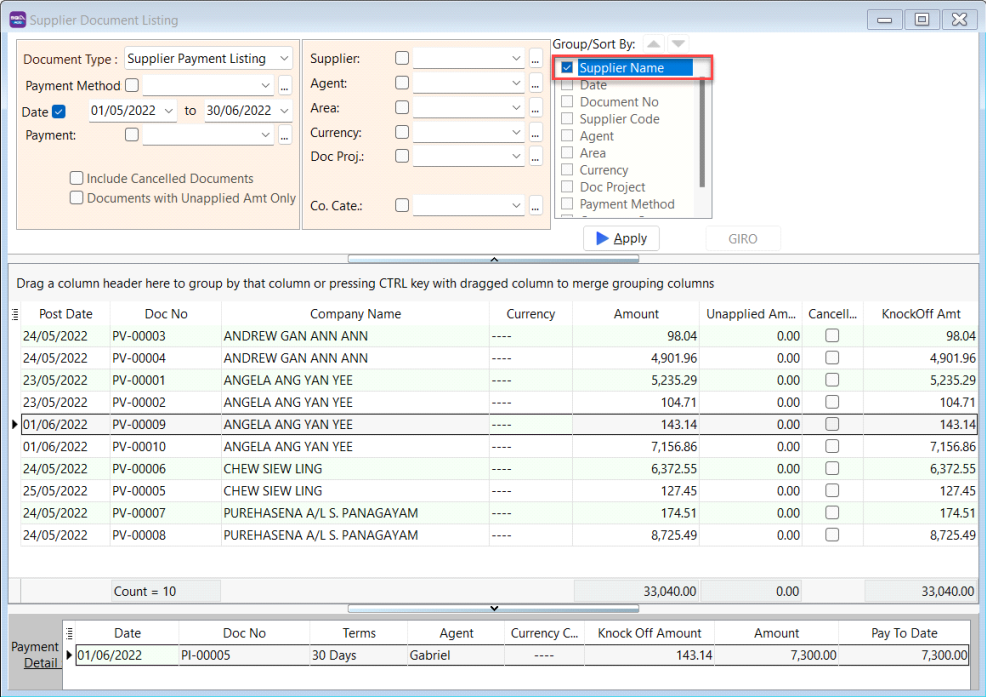

Print CP107, CP107(D), CP58 from Supplier > Supplier Document Listing

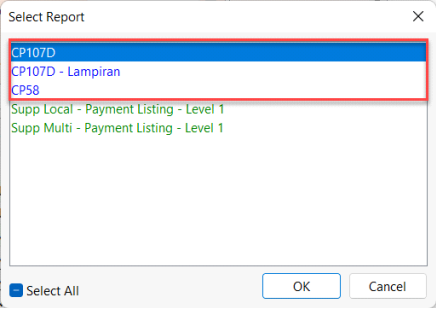

Preview and choose CP107D / Lampiran CP107D / CP58

Related Posts

Access Anytime, Anywhere

Access your account & manage your business anytime, anywhere.

Batch Emails Statements

Email statement to all your customer individually with password encryptions in one simple click.

Special Industries Version

Accountant set, shipping and forwarding, property management, construction, distributor, motor vehicle system, photocopier meter.

Real-Time CTOS Company Overview Reports

Provide SQL Account users a financial standing overview of their customers and suppliers. Helping users make better business risk assessment.

Advance Security Locks

Allowed users access into the documents with restricted by advance level locks, such as hide salaries in cash book.

Intelligence Reporting

Comprehensive reporting such as commission collection reports, tracks your top 3 profitable customers, annual comparison of profit & loss.