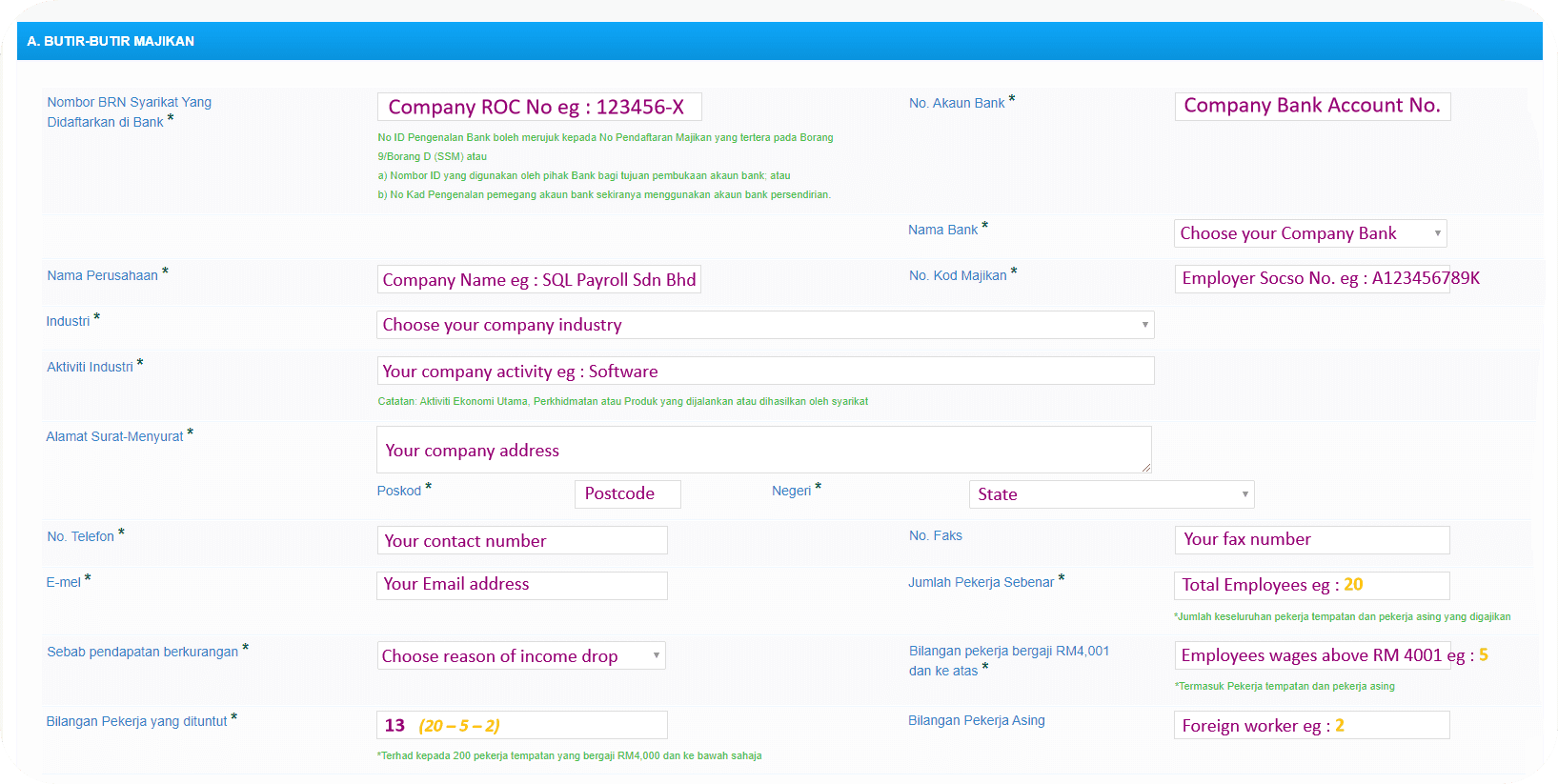

Click here to download the format & fill in manually or, generate it from SQL Payroll directly.

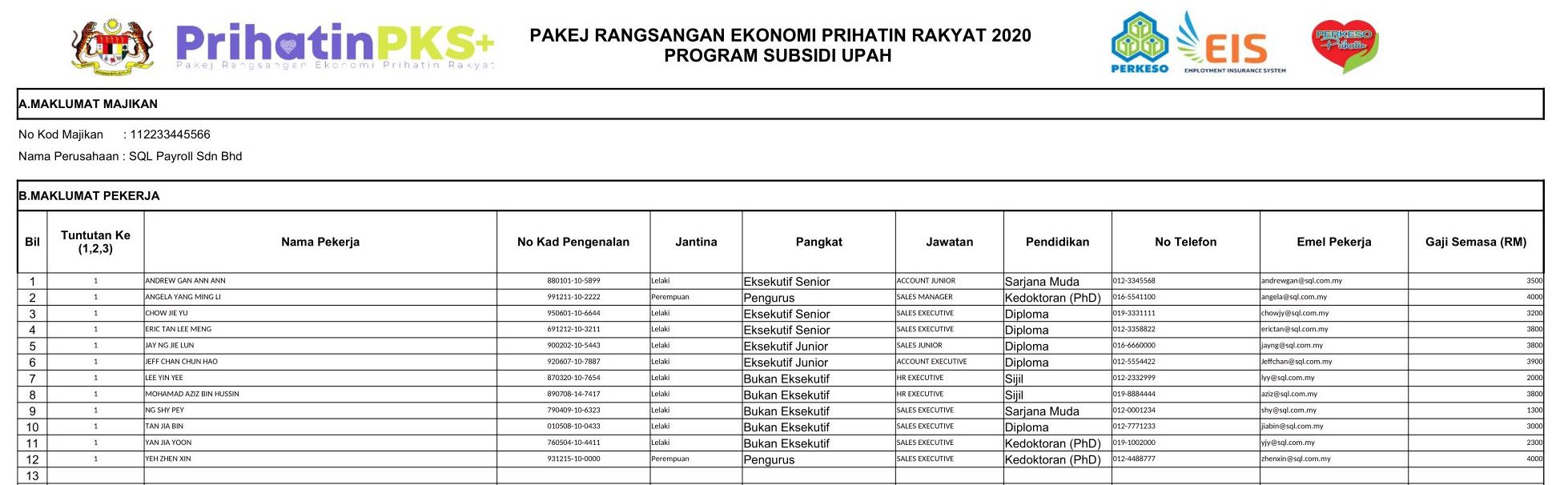

Print directly from SQL Payroll, sign & upload.

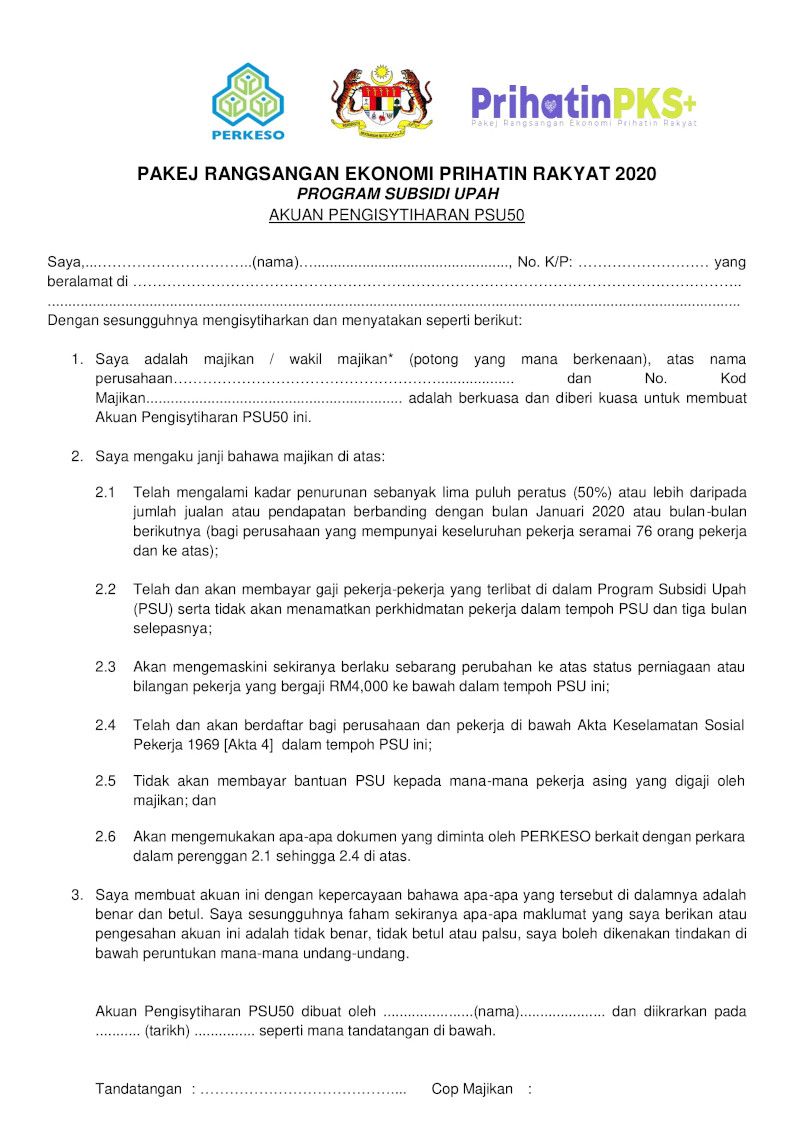

Click here to download the format & fill in manually.

Sample of Employee List

Column Explanation

| No Tuntutan Ke (1,2,3) | 1 = 1st Time Apply, 2 = 2nd Time Apply |

| Name Pekerja | Employee Name |

| No. Kad Pengenalan | Identification Number (I.C No) |

| Jantina | Gender |

| Pangkat | Rank/ Level |

| Jawatan) | Position |

| Pendidikan | Education |

| No. Telefon | Contact Number |

| Email Pekerja | Employee email address |

| Gaji Semasa (RM) | Current Salary (Include OT, Commission, Bonus, Gross Salary) |

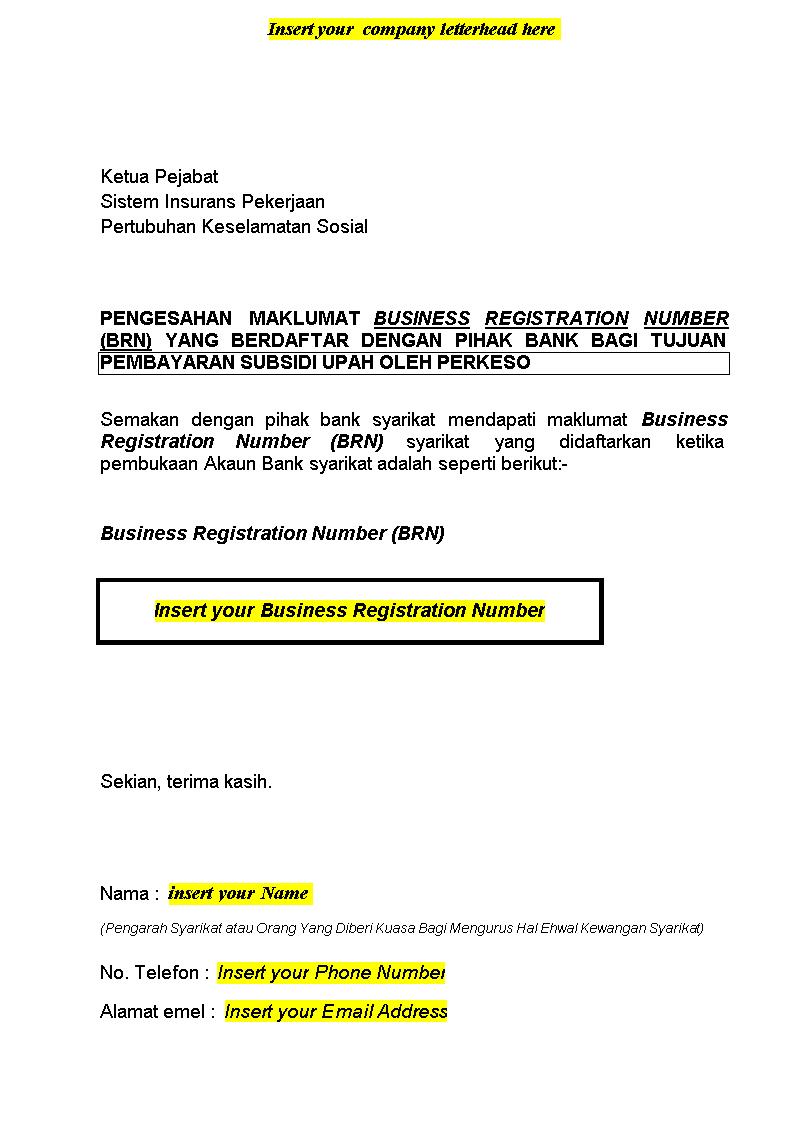

Click on Choose File to upload your company SSM Form, ROS, ROB. Eg, SSM Document such as Sdn Bhd = Form 9.

Click here to download the file. Then fill in your company letterhead, business registration number, your name , your phone number, your email address.

Sample of Bank ID/ MyCOID form

Click on Choose File to upload your company Financial Statement or Sales Report

**This is required if your company number of employees is above 76 pax.

Access Anytime, Anywhere

Access your account & manage your business anytime, anywhere.

Batch Emails Statements

Email statement to all your customer individually with password encryptions in one simple click.

Special Industries Version

Accountant set, shipping and forwarding, property management, construction, distributor, motor vehicle system, photocopier meter.

Real-Time CTOS Company Overview Reports

Provide SQL Account users a financial standing overview of their customers and suppliers. Helping users make better business risk assessment.

Advance Security Locks

Allowed users access into the documents with restricted by advance level locks, such as hide salaries in cash book.

Intelligence Reporting

Comprehensive reporting such as commission collection reports, tracks your top 3 profitable customers, annual comparison of profit & loss.

Certified by Statutory bodies & 100% accurate

Compliant with employment requirements in Malaysia. Inclusive of KWSP, SOCSO, LHDN, EIS, HRDF, EPF Borang A, SOCSO Borang 8A, Income Tax CP39, and Borang E ready. SQL Payroll software is ready to use with minimal setup for all companies.

electronic submission & e-Payment ready

SQL Payroll Software E-submission format are prepared for all banks in Malaysia. Maybank, CIMB, HLBB, Public Bank & many more

Batch email payslip

Securely send payslips to employees using batch email with password encryption

Comprehensive management reports

Print payroll summary, yearly payroll individual report, contribution info report & many more.

Unlimited year records

Records salary info for unlimited amount of years & print EA forms for any year

E Leave mobile app

Apply for leave anytime anywhere with speedy approval from management. Get managerial view of individual leave reports and EA forms